Filters

Introduction

The point made by (Butterworth and Holmes 2002) that ‘the overall profitability of the strategy is seriously impaired by the difficulty, which traders face, in liquidating their positions’ indicates a definite need for more discerning trade selection. This is achieved by using both a standard (threshold) filter and a correlation filter to further refine the various models return/risk characteristics. More encouragingly, in most cases, the application of a filter improves the results of the model, in terms of the out-of-sample Sharpe ratio.

Threshold Filter

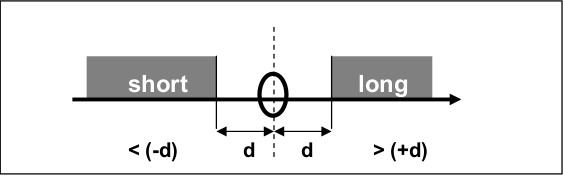

Visual intuition of the threshold filter method. (Dunis et al. 2015)

The standard filter mainly stays out of the market if the predicted change in the spread is smaller in magnitude than X, X being the optimized filter level.

The threshold filter \(X\) is as follows:

if \(\Delta S_t > X\) then go, or stay, long the spread;

if \(\Delta S_t < X\) then go, or stay, short the spread;

if \(-X < \Delta S_t < X\) then stay out of the spread.

where \(\Delta S_t\) is the change in spread and \(X\) is the level of the filter.

Implementation

Example

# Importing packages

import pandas as pd

from arbitragelab.ml_approach.filters import ThresholdFilter

# Getting the dataframe with time series of asset returns

data = pd.read_csv('X_FILE_PATH.csv', index_col=0, parse_dates = [0])

# Calculating spread returns and std dev.

spread_series = data['spread']

spread_diff_series = spread_series.diff()

spread_diff_std = spread_diff_series.std()

# Initializing ThresholdFilter with 2 std dev band for buying and selling triggers.

thres_filter = ThresholdFilter(buy_threshold=-spread_diff_std*2,

sell_threshold=spread_diff_std*2)

std_events = thres_filter.fit_transform(spread_diff_series)

# Plotting results

thres_filter.plot()

Asymmetric Threshold Filter

The asymmetric threshold filter \(X\) is as follows:

if \(\Delta S_t > \vert p_1 \vert * X\) then go, or stay, long the spread;

if \(\Delta S_t < - \vert p_2 \vert * X\) then go, or stay, short the spread;

if \(- \vert p_2 \vert * X < \Delta S_t < \vert p_1 \vert * X\) then stay out of the spread.

where \(\Delta S_t\) is the change in spread, \(X\) is the level of the filter and \((p_1, p_2)\) being coefficients estimated from the TAR model.

Example

# Importing packages

import pandas as pd

from arbitragelab.ml_approach.filters import ThresholdFilter

# Getting the dataframe with time series of asset returns

data = pd.read_csv('X_FILE_PATH.csv', index_col=0, parse_dates = [0])

# Calculate spread returns and std dev.

spread_series = data['spread']

spread_diff_series = spread_series.diff()

spread_diff_std = spread_diff_series.std()

# Initialize the TAR asymmetry coefficients.

p_1 = -0.012957

p_2 = -0.038508

buy_thresh = abs(p_1) * spread_diff_std*2

sell_thresh = - abs(p_2) * spread_diff_std*2

# Initialize ThresholdFilter with asymmetric buying and selling triggers.

asym_thres_filter = ThresholdFilter(buy_threshold=buy_thresh,

sell_threshold=sell_thresh)

std_events = asym_thres_filter.fit_transform(spread_diff_series)

# Plotting results

asym_thres_filter.plot()

Correlation Filter

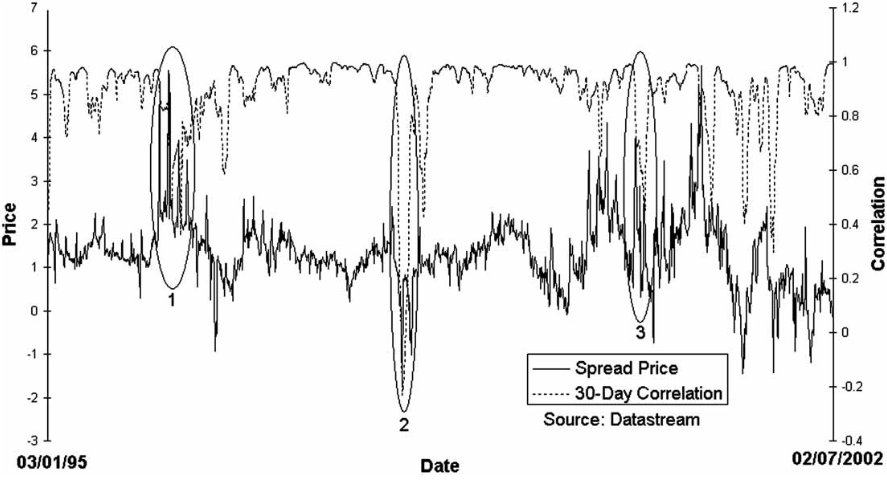

Side by side comparison of the legs correlation and the spread. (Dunis et al. 2015)

As well as the application of a standard filter, trades can also be filtered in terms of correlation. This is presented as a new methodology to filter trading rule returns on spread markets. The idea is to enable the trader to filter out periods of static spread movement (when the correlation between the underlying legs is increasing) and retain periods of dynamic spread movement (when the correlation of the underlying legs of the spread is decreasing).

By using this filter, it should also be possible to filter out initial moves away from the fair value, which are generally harder to predict than moves back to fair value. Doing this also filters out periods when the spread is stagnant.

Formally, the correlation filter \(X_c\) can be written as:

if \(\Delta C < X_c\) then take the decision of the trading rule;

if \(\Delta C > X_c\) then stay out of the market.

where \(\Delta C\) is the change in correlation and \(X_c\) being the size of the correlation filter.

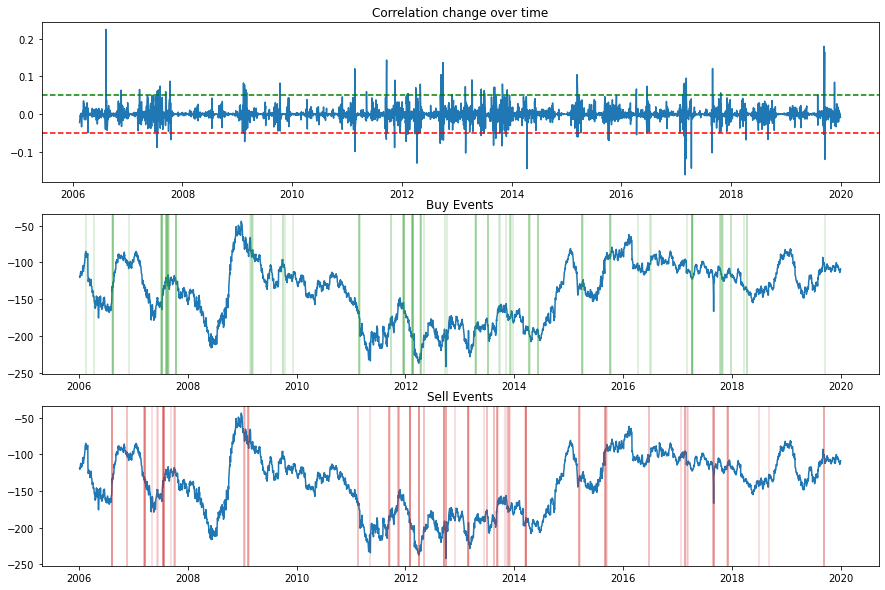

Example plot from a fitted CorrelationFilter class.

Implementation

Example

# Importing packages

import pandas as pd

from arbitragelab.ml_approach.filters import CorrelationFilter

# Getting the dataframe with time series of asset returns

data = pd.read_csv('X_FILE_PATH.csv', index_col=0, parse_dates = [0])

# Initialize CorrelationFilter with thresholds of -0.05 and 0.05.

corr_filter = CorrelationFilter(buy_threshold=0.05, sell_threshold=-0.05, lookback=30)

corr_filter.fit(data[['leg_1', 'leg_2']])

corr_events = corr_filter.transform(data[['leg_1', 'leg_2']])

# Plotting results

corr_filter.plot()

Volatility Filter

(Dunis, Laws, and Middleton 2011), develop a refined volatility filter in order to offer a more sophisticated insight into market timing.

The intuition of the method is to avoid trading when volatility is very high while at the same time exploiting days when the volatility is relatively low. The significant difference between market timing techniques as used in (Dunis, Laws, and Middleton 2011) and time-varying leverage as implemented here is that leverage can be easily achieved by scaling position sizes inversely to computed risk measures.

There are a number of different measurement techniques available to analysts when calculating time-varying volatility. The most common method is the calculation of a moving average as used by (Dunis and Miao 2006) who estimate volatilities using a fixed window of time (number of days, weeks, months). The same volatility regime classification technique was employed for the purpose of this research.

The RiskMetrics volatility can be seen as a special case of the (Bollerslev 1986) GARCH model with pre-determined decay parameters, and it is calculated using the following formula

where \(\sigma^2\) is the volatility forecast of a specific asset, \(r^2\) is the squared return of that asset, and \(\mu = 0.94\) for daily data and \(0.97\) for monthly data, as computed in (Morgan 1994).

Following (Morgan 1994), the estimation of volatility regimes is therefore based on a rolling historical average of RiskMetrics volatility (\(\mu_{AVG}\)) as well as the standard deviation of this volatility (\(\sigma\)). The latter is in essence ‘the volatility of the volatility’. For the purpose of this investigation, both historical parameters \(\mu_{AVG}\) and \(\sigma\) are calculated on a three-month rolling window. The average of both \(\mu_{AVG}\) and \(\sigma\) are then calculated based on these three-month historic periods.

For instance, the historical volatilities for our in-sample data are calculated over a total 16 periods with each spanning 3 months in duration. Thus, volatility regimes are then classified based on both the average totals for \(\mu\) and \(\sigma\) over this time period.

Volatility regimes are categorised as

Lower High - (between \(\mu_{AVG}\) and \(\mu_{AVG} + 2\sigma\) )

Medium High - (between \(\mu_{AVG} + 2\sigma\) and \(\mu_{AVG} + 4\sigma\) )

Extremely High - (greater than \(\mu_{AVG} + 4\sigma\) )

Similarly, periods of lower volatility are categorised as

Higher Low - (between \(\mu_{AVG}\) and \(\mu_{AVG} - 2\sigma\) )

Medium Low - (between \(\mu_{AVG} - 2\sigma\) and \(\mu_{AVG} - 4\sigma\) )

Extremely Low - (less than \(\mu_{AVG} - 4\sigma\) )

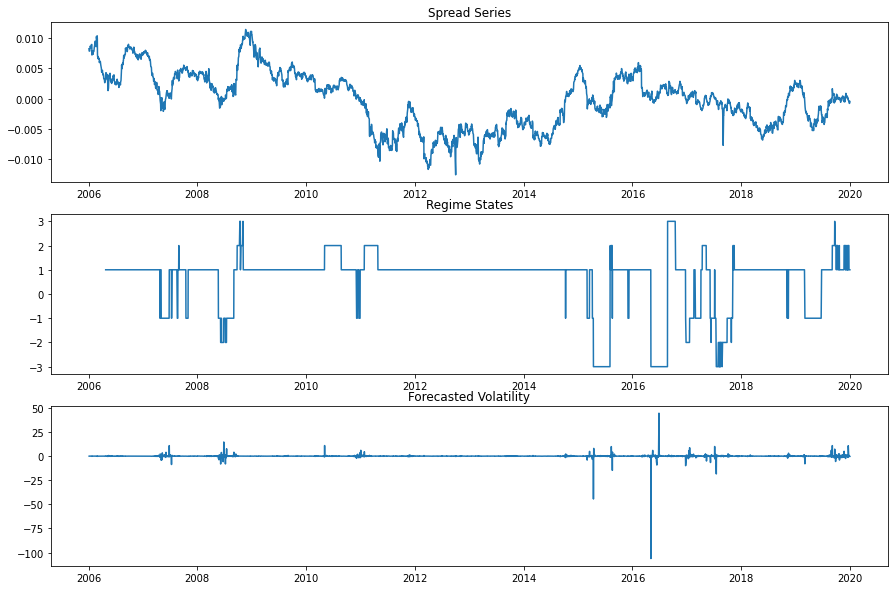

Example plot from a fitted VolatilityFilter class.

Implementation

Example

# Importing packages

import pandas as pd

from arbitragelab.ml_approach.filters import VolatilityFilter

# Getting the dataframe with time series of asset returns

data = pd.read_csv('X_FILE_PATH.csv', index_col=0, parse_dates = [0])

spread_series = data['spread']

# Initialize VolatilityFilter a 30 period lookback parameter.

vol_filter = VolatilityFilter(lookback=30)

vol_events = vol_filter.fit_transform(spread_series)

# Plotting results

vol_filter.plot()