Welcome to the Statistical Arbitrage Laboratory

What was only possible with the help of huge R&D teams is now at your disposal, anywhere, anytime.

ArbitrageLab is a python library that includes both end-to-end strategies and strategy creation tools that cover the whole range of strategies defined by Krauss’ taxonomy for pairs trading strategies.

Hudson & Thames documentation has three core advantages in helping you learn the new techniques: Thoroughness, Flexibility and Credibility.

Thoroughness

We want to make the learning process for the advanced tools and approaches effortless for our clients by providing detailed explanations, examples of use and additional context behind them.

The general documentation structure looks the following way:

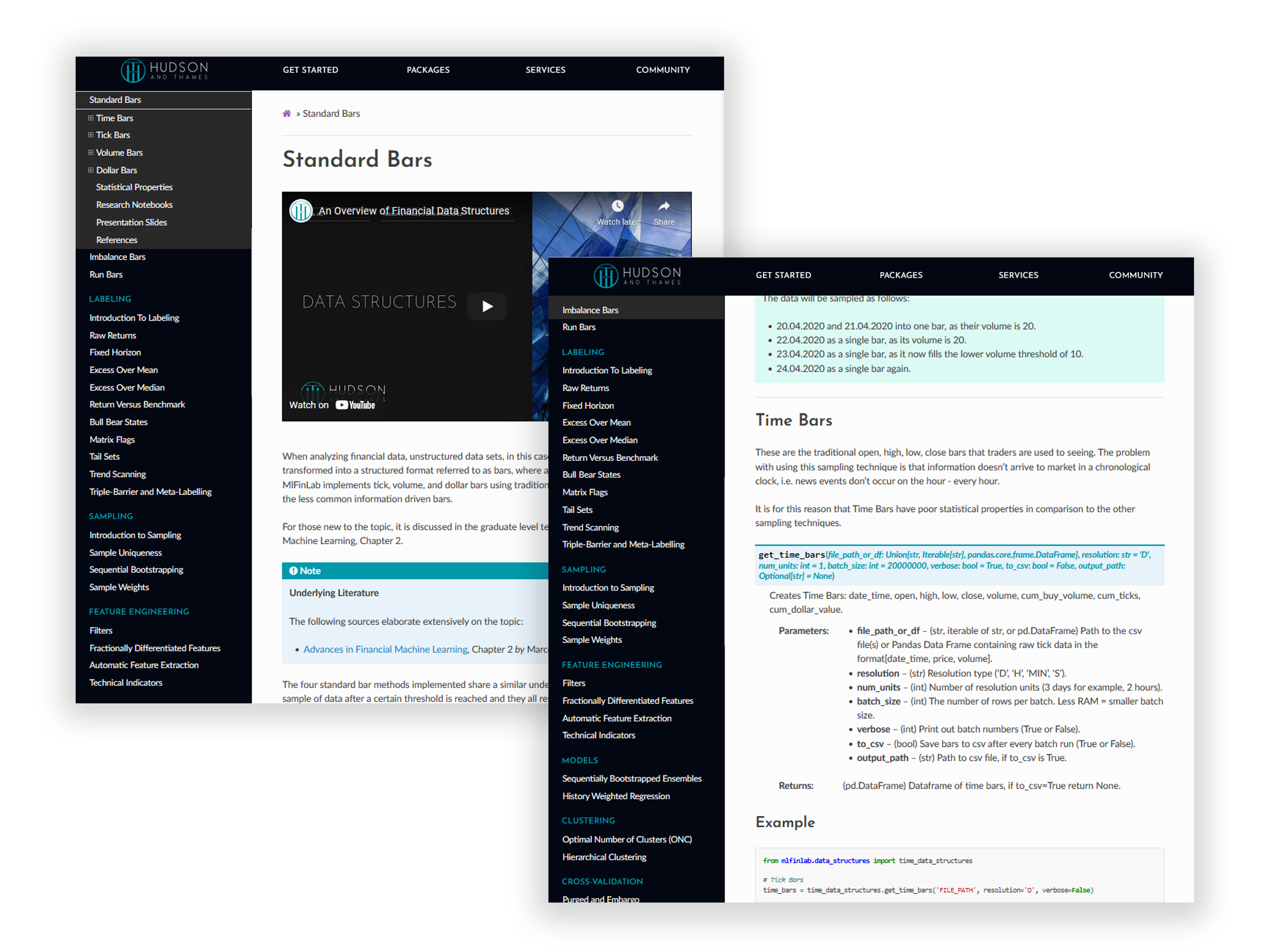

Documentation page : |

|---|

Lecture video* |

Mathematical concept explanation |

Implementation description |

Short code example |

Link to an extensive example notebook |

Presentation slides* |

Flexibility

Learn in the way that is most suitable for you as more and more documentation pages are now supplemented with both video lectures and presentation slides on the topic.

Credibility

All of our implementations are from the most elite and peer-reviewed journals.

Including publications from:

Who is Hudson & Thames?

Hudson and Thames Quantitative Research is a company with the goal of bridging the gap between the advanced research developed in quantitative finance and its practical application. We have created three premium python libraries so you can effortlessly access the latest techniques and focus on what matters most: creating your own winning strategy.

License

This project is open-source, following the BSD 3 license.

API Reference